Still confused about high-frequency trading? Yes.

This piece originally appeared as a guest post on Noahpinion. Professor ‘Pinion graciously offered me a platform to continue hoo-ha’ing. I obliged.[1]

I’ve felt like a popular boy lately. In the five years I’ve been developer and researcher at a small trading firm, my family and friends mostly thought I just look at numbers, write code, and play with computers all day; they thought mostly correctly. But Michael Lewis’ recent indictment of high-frequency trading (HFT) changed all that. Now the mystique of “the black box” pervades the blogosphere and news media. I’m often asked for my thoughts about so-and-so’s piece or if regulation is going to kill my job. Discerning readers wont be surprised when I say that most reporting on this topic falls somewhere between incomplete and wrong.

Today Evan Soltas published an introduction to high-frequency trading on Ezra Klein’s new Vox Media: Confused about high-frequency trading? Here’s a guide. But rather than a guide to HFT, it’s only a guide to the narrow set of topics made popular by Lewis’ book — which pertain only to US equities are not representative of the whole field. While this critique could easily be applied to most of the recent HFT coverage, Mr. Soltas is a very clear writer and that makes it easy to do a point-by-point analysis. Each of the subject headings below corresponds to the respective heading in the Vox piece.

(As I preface all of my pieces: there is a non-zero probability that I err. My focus as a developer has been primarily in futures and currency markets. While currencies are fragmented similar to US equities, there are specific nuances and regulations of which I do not have experience)

What is high-frequency trading?

… High-frequency trading is a kind of market activity that moves in less than one millisecond to spot and take advantage of an opportunity to buy or sell. It happens through trading algorithms, programs that determine how to trade based on fast-moving market data. …

In this section we learn that HFT is faster than blinking, what type of market activity it analyzes, and a type of trade it might make. But we don’t get a precise definition of what it is. Allow me.

high-frequency trading: the ability to quickly execute trades and manage order activity.

This is a broad definition because the field is broad. Loosely, the three main categories of automated trading strategies are (1) latency arbitrage, (2) market making, and (3) statistical arbitrage. There are many algorithmic firms employing many different strategies that fall into some combination of the above. However, it is important to note that none of these strategies are risk free and thus arbitrage, by the economic definition, is a misnomer. Unfortunately, Mr. Lewis has pigeonholed the entire industry into number one. And number one is very boring.

(I’m not going to talk about (2) and (3) in this post. Maybe some time in the future. But I really hope this is my last piece on trading for a while. I think about other stuff too, dammit!)

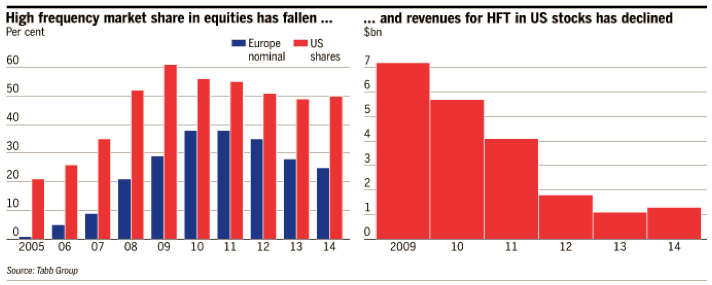

Is high-frequency trading growing?

Not anymore, according to most data. High-frequency trading came into vogue during the 2000s, but after many traders entered the market, profits are way down, and there seems to be slightly less high-frequency trading than there used to be …

Here Soltas conflates the decline in firm profits with the incidence of HFT itself. This is odd because in economic terms, a perfectly competitive market implies that long term profits will be zero. This is exactly what we would expect to see as competition increases.

Generally, academic research pertaining to HFT firms uses the SEC (2010) definition:

HFT firm: market participants that end the day with close to zero inventories, frequently submit and cancel limit orders, use co-location facilities and highly efficient algorithms, and have short holding periods.

While this is a good definition for HFT-only firms, the declining costs of co-located servers, declining costs of latency-based solutions from software and hardware manufacturers, and the increase in the amount of open source projects has broadened the ability for any firm to do HFT-style execution. The industry magazine Automated Trader frequently covers the fast execution algorithms which have allowed firms to get into large positions with minimal impact on market prices — meaning less opportunities for other firms to capitalize on. (Last I heard, the market rate for a custom high-frequency platform is $2-4 million)

So yes, high-frequency trading is growing even if HFT-only firm profits are decreasing.

How does high-frequency trading make money?

… When the traders see CalPERS place a bid for Apple shares on the tech-heavy Nasdaq exchange, they quickly buy shares on other exchanges, inferring that CalPERS’ orders are coming down the wires. Then the high-frequency traders sell the Apple shares back to CalPERS at a higher price than they paid for them a millisecond ago. This “electronic front-running” happens because the high-frequency traders have an advantage in terms of speed, and because “the stock market” doesn’t really exist — what exists are many stock exchanges in a trading network. …

… The third exploits the network structure of markets, and the fact that they don’t all adjust instantly to changes in price. If high-frequency traders can figure out where a stock price will be in the next millisecond before other investors can get a quote, that’s a huge advantage they can use for profit.

Yes and no. Yes, that is roughly the trade Mr. Lewis describes in his book. But the reality is a bit more nuanced. First, I think it’s unlikely that CalPERS has a Market Participant Identification (MPID) on the NASDAQ OMX, so these traders wouldn’t identify the orders as belonging to CalPERS (from their website it looks like they conduct their trading through various brokers).

More importantly, neither of those trades are risk free. In the first case, firms are making bets that someone is trying to get into a large position and will pay whatever price is offered. In the second, they are betting that the price change they witnessed on one exchange is actually where the market is going to be. Here’s an example:

Imagine these are the order books (i.e. the sets of bids and offers by price and size) for the same stock on two different markets. The HFT firm sees someone place a buy order for 2 on Market A at 16127 (making that price the new best bid with a quantity of 1). So the HFT firm does the same on Market B. Now in order to profit from that movement, they have to be able to sell it at a higher price. If someone else comes in and starts selling, forcing the price downward, the HFT firm will lose money on that bet.

Can high-frequency trading cause stock-market crashes?

The high-frequency trading algorithms simply move too fast for humans to intervene with better judgment. When stocks drop, the trading programs may decide to stop trading, withdrawing liquidity from the market, or they may add to the sell-off.

This supposes that humans do have better judgement. But market crashes have happened long before the existence of HFT. In a previous post, I noted that even completely automated firms have people, called operations or “ops”, who monitor the overall health of the systems to make sure they are functioning as desired. When something out of the ordinary happens, they have to quickly figure out whether or not to turn off certain algorithms. No one flips the switch and shuts their eyes (except some people working night desk, *cough* *cough*).

That wouldn’t surprise many people who remember what happened to the stock market on May 6, 2010 at 2:45 p.m. — the “Flash Crash,” in which U.S. stocks fell 9 percent and then recovered in the course of a few minutes. Shares in companies like Accenture, a management consultancy, fell from $40 a share to a penny.

Oh the good ole Flash Crash. Amid all of the phenomenology reports and finger pointing, it’s easy to forget the general conditions surrounding the event. There was massive political uncertainty and the markets were already volatile. All morning, CNBC had a picture-in-picture box of the riots in Greece. Further, it’s a bit disingenuous to say share prices fell to a penny. All that implies is that there were no orders in the order book — very little trading actually took place at the low prices. During an equivalent panic in the days of floor traders, no one would raise a hand to trade.

What caused the overloading, Nanex argues, was “quote stuffing” — high-frequency traders that sent in a blizzard of orders to buy and sell at the same time, only to cancel those orders milliseconds later before they went through.

I’m highly skeptical of Nanex’s data and methodologies. Like all of their claims, the “quote stuffing” scenario has never been validated. Analysis that comes from them should not be treated like peer-reviewed research.

Are there other possible problems with high-frequency trading?

1) Much high-frequency trading exploits data before it is public for an advantage.

Until last summer, the data firm Thomson Reuters, for example, sold to elite investors the right to see an important economic statistic, the University of Michigan’s consumer confidence survey, five minutes earlier than the rest of the market. An “even-more elite” group of high-frequency trading clients could purchase an extra 500 millisecond head start.

Important economic statistics are released on regularly scheduled dates and times. Market participants know these well in advance. If a firm conducts trading that is sensitive to an economic number, the firm appropriately removes bids and offers from the market, and possibly closes its position, prior to the number’s release. There’s very little advantage to be had.

What are some ways we could curb high-frequency trading?

The proposed ideas in this section are pretty awful — not to mention the endless amount of unintended consequences that comes with any idea to “redesign the way markets work.”

But I will say Finem Respice — look to the end. There are many electronic markets in the world that trade under many different sets of rules. We should seek solutions that are already in use in real markets. The currency exchange EBS has successfully experimented with several ideas. First, after they increased the minimum price increment (tick size) of several currency pairs, they noticed more liquidity at every price level. More recently, they’ve introduced latency floors which randomize a queue of incoming messages in several millisecond buckets. That has also been a success and they are expanding it to all of their products.

Fin

I appreciate all of the responses (positive and negative) that I’ve received through email, twitter and the comments on Noahpinion. There are definitely a lot of talented people thinking about this topic right now. So I’m going to pass the buck. Cheers.